All About Living in Flood Zones in Downtown Charleston

With hurricane season upon us, I thought this would be the opportune time to talk about living in flood zones in Downtown Charleston. Being in a flood zone is a fact of life for us here, because, uh…we are a peninsula completely surrounded by water. But there are nuances to it you should know about – 1. FEMA flood zones, and 2. Localized flooding. One has to do with the cost of insurance, the other has to do with the convenience of getting around – there’s even a new t-shirt company by the name of Flooded Streets, in homage to this peculiar quirk of living Downtown.

FEMA Flood Zones

So let’s start with the big stuff. Hurricanes! Fear of hurricanes hitting us is one of the most frequently expressed concerns of my clients moving here from other places. Understandable, yet frankly, overwrought. In the 12 total years I have lived in Charleston, only once was there threat of a Category 3+ and it ended up zooming right by us. (Though you know of course since I am writing about this now, 2013 will be the year we get hit.)

But I digress…rather than look to me for the probability of a hurricane hit, let’s look to the experts. Here’s an excerpt from an excellent Post and Courier article from last year about flood insurance and the likelihood of a BIG HIT from a hurricane in our area.

“Enough Already With The Fear-Mongering”

A storm is brewing in the Atlantic; forecasters are fanning out along its projected path; it has a name. Beryl. Floyd. Hugo. Time for a gut check: Does your stomach tighten? After all, isn’t South Carolina a hurricane magnet?

Maybe not.

South Carolina’s vulnerability to hurricanes is much more nuanced than the headlines on the Weather Channel might suggest. Experts say based on historical trends, minimal hurricane-force winds or higher will touch some part of South Carolina every five years.

Minimal hurricanes typically aren’t catastrophes. It’s the Category 3 and above storms that knock a city off its foundation. The 60-mile area around Charleston has seen only two of these since 1851 (Hugo and the Hurricane of 1893).

Narrow the location even more, and the situation is even less worrisome. A Post and Courier report showed that when analysts study a specific location’s vulnerability, a coastal property owner would on average see catastrophic winds every 370 years or longer.

Now that doesn’t sound so drastic does it? Frankly, if I had to pick a natural disaster, I’d pick a hurricane over a tornado, earthquake, tsunami or mudslide any day. Why? Because you have time to get the heck out of its way.

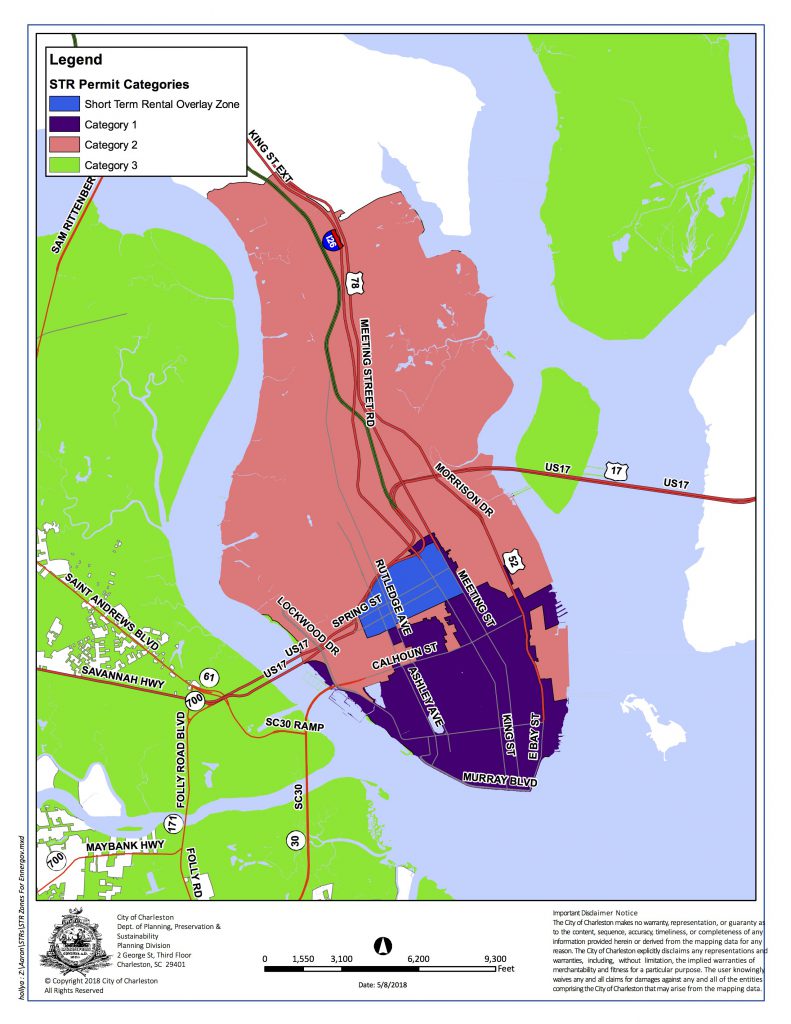

Anyway, FEMA sets its flood maps and insurance requirement based on cumulative probabilities, height of the land and proximity to water. There are lots of classifications, but the two we see most commonly on the Charleston Peninsula are AE and X.

AE Defined – Areas subject to inundation by the 1-percent-annual-chance flood event determined by detailed methods. Base Flood Elevations (BFEs) are shown. Mandatory flood insurance purchase requirements and floodplain management standards apply.

X Defined – Areas of minimal flood hazard, which are the areas outside the SFHA and higher than the elevation of the 0.2-percent-annual-chance flood.

In this graphic below – only the white spots are in the X zone.

These few homes in the X zone do not require flood insurance, though most people elect to purchase the minimal insurance, which usually costs less than $500 per year. This rate compares to what you pay insurance companies when you live anywhere in the purple area, or an amount I’ll describe as “OUT THE WAZOO”, whether you ever see flooding in your lifetime at that particular house or not.

That is, unless the house happens to be one of the lucky ones built up, or on a hill (yes, we have a few of those in Charleston), or if it is newer construction., in which case FEMA requires that you build the house above the base elevation. For example, most of the peninsula is in AE 13 – meaning a house must be built 13 feet above sea level. This is why much of Lowcountry architecture features the garage underneath the house, or very high crawl spaces. And then there’s also the conversation of flood-venting which can also affect your insurance rates. Do the cumulative square inches of the vents in your crawl space equal the square footage of the first floor of your house? And are they positioned properly – on opposing or perpendicular sides??? It’s all quite detailed – and I usually work with the insurance company and surveyor to help you figure it out.

Localized Flooding

So, moving on to Point #2 – the localized flooding – or what we see when the combination of heavy rains and high tides (and watch out if the full moon is in the mix too!) is just right…er…wrong. Remember, not only are we called the Lowcountry for a very good reason, but also much of our city was built directly on top of water. For example, Market Street was once a river, which is why during one of the worst rain/high tide combos we’ve seen in 15 years happened back in August 2012, some people delighted in doing this.

Kayaking through the Market. Thanks for the fantastic photo Charleston City Paper and Charles Merry!

Yes. That is real. That is not photoshopped. We mostly take this localized flooding with a grain of salt and a tad of good humour around here, put on our Wellies and try NOT to drive in the areas we know to have impassable puddles unless we have a huge SUV. Here’s a crowd-sourced map about the flood prone streets which I posted on this blog more than four years ago. It’s still useful but not quite accurate because for some reason, the flooding shifts around.

View Downtown Charleston, SC flood-prone streets in a larger map

So there’s the explanation of downtown flooding in a nutshell – or blog post as it were. I’ll leave you with a little video I took of a river of water gushing into Colonial Lake last August. Crazy!

Previous Post

Previous Post Next Post

Next Post

You should mention the 30 wait for new flood policies to go into effect and the difference in rates for owner occupied vs. second/vacation homes.

Thanks Robert! You are right that there are even more nuances I didn’t address. And everything will change even further this fall. It’s complicated!!